Stop/Take BoundsThe Stop/Take Bounds indicator is tool for setting dynamic stop-loss and take-profit levels based on percentage distance from the price. Unlike traditional ATR-based methods, this indicator allows traders to set stop levels as a fixed percentage of the price and define the take-profit multiple.

- Stop-loss distanceis determined as a percentage of the current price (e.g., 1% means the stop-loss is always 1% away from the price).

- Take-profit distance is calculated by multiplying the stop-loss distance by a user-defined multiplier (e.g., a multiplier of 2 places the take-profit level twice as far as the stop-loss).

- The indicator plots red lines for stop-loss levels and green lines for take-profit levels, making it easy to visualize risk-to-reward scenarios.

How to Use

1. Set Stop-Loss Distance (%) – Define how far the stop-loss should be from the price.

2. Set Take-Profit Multiplier – Choose how many times larger the take-profit should be compared to the stop-loss.

3. Apply to Long and Short Trades – The indicator automatically plots levels for both long and short positions.

4. Use in Manual or Algorithmic Trading – Ideal for discretionary traders as well as for integration into algorithmic strategies.

Use Cases

- Risk Management – Helps maintain disciplined risk-to-reward ratios.

- Strategy Development – Can be used in the creation of algorithmic trading systems.

- Trailing Stop Simulation – Can act as a trailing stop mechanism when used dynamically.

This indicator is a great addition to any trading strategy!

"Trailing stop" için komut dosyalarını ara

4Vietnamese 3x SupertrendThis strategy attempts to capture long positions in the Vietnamese stock market using a combination of three Supertrend indicators and additional filters. It utilizes pyramiding to enter up to three long positions with a 33.33% allocation each.

Key Elements:

Supertrend Indicators: Three Supertrend indicators are used with different lengths and multipliers to identify potential trend changes.

Entry Conditions:

The strategy looks for a downtrend on the slowest Supertrend (Supertrend3) followed by uptrends on the medium (Supertrend2) and fast (Supertrend1) Supertrends.

Alternatively, if Supertrend3 is still downtrending, but Supertrend1 is downtrending and a significant previous high (highestGreen) exists, an entry signal is generated.

An optional filter allows using the highest of the last two red candles for highestGreen calculation.

Entry Stop Loss:

An optional stop loss can be set based on the entry price of previous long positions, preventing further losses if the price falls below entry prices.

Exit Conditions:

Three exit options are available:

- All Downtrend Exit: Close all positions if all Supertrends turn uptrend and a bearish candlestick pattern (close price lower than open price) is formed.

- Average Price in Loss Exit: Close all positions if the average entry price of open positions is higher than the current closing price (indicating a loss).

- All Positions in Loss Exit: Close all positions if any of the following conditions are met:

A single open position exists, and its entry price is higher than the current close price.

Two open positions exist, and their entry prices are both higher than the current close price.

Three open positions exist, and their entry prices are all higher than the current close price.

Pyramiding: The strategy allows entering up to three long positions with a fixed allocation of 33.33% each.

Customization Options:

The strategy provides various input parameters to customize its behavior:

Supertrend lengths and multipliers for each indicator.

Option to use the highest of the last two red candles for highestGreen calculation.

Enabling/disabling Entry Stop Loss and different exit conditions.

Further Enhancements:

Explore additional entry and exit filters to refine trade signals.

Consider incorporating risk management techniques like position sizing and trailing stops.

Backtest the strategy with historical data to evaluate its effectiveness and identify potential areas for improvement.

Stoch RSI and RSI Buy/Sell Signals with MACD Trend FilterDescription of the Indicator

This Pine Script is designed to provide traders with buy and sell signals based on the combination of Stochastic RSI, RSI, and MACD indicators, enhanced by the confirmation of candle colors. The primary goal is to facilitate informed trading decisions in various market conditions by utilizing different indicators and their interactions. The script allows customization of various parameters, providing flexibility for traders to adapt it to their specific trading styles.

Usefulness

This indicator is not just a mashup of existing indicators; it integrates the functionality of multiple momentum and trend-detection methods into a cohesive trading tool. The combination of Stochastic RSI, RSI, and MACD offers a well-rounded approach to analyzing market conditions, allowing traders to identify entry and exit points effectively. The inclusion of color-coded signals (strong vs. weak) further enhances its utility by providing visual cues about the strength of the signals.

How to Use This Indicator

Input Settings: Adjust the parameters for the Stochastic RSI, RSI, and MACD to fit your trading style. Set the overbought/oversold levels according to your risk tolerance.

Signal Colors:

Strong Buy Signal: Indicated by a green label and confirmed by a green candle (close > open).

Weak Buy Signal: Indicated by a blue label and confirmed by a green candle (close > open).

Strong Sell Signal: Indicated by a red label and confirmed by a red candle (close < open).

Weak Sell Signal: Indicated by an orange label and confirmed by a red candle (close < open).

Example Trading Strategy Using This Indicator

To effectively use this indicator as part of your trading strategy, follow these detailed steps:

Setup:

Timeframe : Select a timeframe that aligns with your trading style (e.g., 15-minute for intraday, 1-hour for swing trading, or daily for longer-term positions).

Indicator Settings : Customize the Stochastic RSI, RSI, and MACD parameters to suit your trading approach. Adjust overbought/oversold levels to match your risk tolerance.

Strategy:

1. Strong Buy Entry Criteria :

Wait for a strong buy signal (green label) when the RSI is at or below the oversold level (e.g., ≤ 35), indicating a deeply oversold market. Confirm that the MACD shows a decreasing trend (bearish momentum weakening) to validate a potential reversal. Ensure the current candle is green (close > open) if candle color confirmation is enabled.

Example Use : On a 1-hour chart, if the RSI drops below 35, MACD shows three consecutive bars of decreasing negative momentum, and a green candle forms, enter a buy position. This setup signals a robust entry with strong momentum backing it.

2. Weak Buy Entry Criteria :

Monitor for weak buy signals (blue label) when RSI is above the oversold level but still below the neutral (e.g., between 36 and 50). This indicates a market recovering from an oversold state but not fully reversing yet. These signals can be used for early entries with additional confirmations, such as support levels or higher timeframe trends.

Example Use : On the same 1-hour chart, if RSI is at 45, the MACD shows momentum stabilizing (not necessarily negative), and a green candle appears, consider a partial or cautious entry. Use this as an early warning for a potential bullish move, especially when higher timeframe indicators align.

3. Strong Sell Entry Criteria :

Look for a strong sell signal (red label) when RSI is at or above the overbought level (e.g., ≥ 65), signaling a strong overbought condition. The MACD should show three consecutive bars of increasing positive momentum to indicate that the bullish trend is weakening. Ensure the current candle is red (close < open) if candle color confirmation is enabled.

Example Use : If RSI reaches 70, MACD shows increasing momentum that starts to level off, and a red candle forms on a 1-hour chart, initiate a short position with a stop loss set above recent resistance. This is a high-confidence signal for potential price reversal or pullback.

4. Weak Sell Entry Criteria :

Use weak sell signals (orange label) when RSI is between the neutral and overbought levels (e.g., between 50 and 64). These can indicate potential short opportunities that might not yet be fully mature but are worth monitoring. Look for other confirmations like resistance levels or trendline touches to strengthen the signal.

Example Use : If RSI reads 60 on a 1-hour chart, and the MACD shows slight positive momentum with signs of slowing down, place a cautious sell position or scale out of existing long positions. This setup allows you to prepare for a possible downtrend.

Trade Management:

Stop Loss : For buy trades, place stop losses below recent swing lows. For sell trades, set stops above recent swing highs to manage risk effectively.

Take Profit : Target nearby resistance or support levels, apply risk-to-reward ratios (e.g., 1:2), or use trailing stops to lock in profits as price moves in your favor.

Confirmation : Align these signals with broader trends on higher timeframes. For example, if you receive a weak buy signal on a 15-minute chart, check the 1-hour or daily chart to ensure the overall trend is not bearish.

Real-World Example: Imagine trading on a 15-minute chart :

For a buy:

A strong buy signal (green) appears when the RSI dips to 32, MACD shows declining bearish momentum, and a green candle forms. Enter a buy position with a stop loss below the most recent support level.

Alternatively, a weak buy signal (blue) appears when RSI is at 47. Use this as a signal to start monitoring the market closely or enter a smaller position if other indicators (like support and volume analysis) align.

For a sell:

A strong sell signal (red) with RSI at 72 and a red candle signals to short with conviction. Place your stop loss just above the last peak.

A weak sell signal (orange) with RSI at 62 might prompt caution but can still be acted on if confirmed by declining volume or touching a resistance level.

These strategies show how to blend both strong and weak signals into your trading for more nuanced decision-making.

Technical Analysis of the Code

1. Stochastic RSI Calculation:

The script calculates the Stochastic RSI (stochRsiK) using the RSI as input and smooths it with a moving average (stochRsiD).

Code Explanation : ta.stoch(rsi, rsi, rsi, stochLength) computes the Stochastic RSI, and ta.sma(stochRsiK, stochSmoothing) applies smoothing.

2. RSI Calculation :

The RSI is computed over a user-defined period and checks for overbought or oversold conditions.

Code Explanation : rsi = ta.rsi(close, rsiLength) calculates RSI values.

3. MACD Trend Filter :

MACD is calculated with fast, slow, and signal lengths, identifying trends via three consecutive bars moving in the same direction.

Code Explanation : = ta.macd(close, macdLengthFast, macdLengthSlow, macdSignalLength) sets MACD values. Conditions like macdLine < macdLine confirm trends.

4. Buy and Sell Conditions :

The script checks Stochastic RSI, RSI, and MACD values to set buy/sell flags. Candle color filters further confirm valid entries.

Code Explanation : buyConditionMet and sellConditionMet logically check all conditions and toggles (enableStochCondition, enableRSICondition, etc.).

5. Signal Flags and Confirmation :

Flags track when conditions are met and ensure signals only appear on appropriate candle colors.

Code Explanation : Conditional blocks (if statements) update buyFlag and sellFlag.

6. Labels and Alerts :

The indicator plots "BUY" or "SELL" labels with the RSI value when signals trigger and sets alerts through alertcondition().

Code Explanation : label.new() displays the signal, color-coded for strength based on RSI.

NOTE : All strategies can be enabled or disabled in the settings, allowing traders to customize the indicator to their preferences and trading styles.

Entropy-Based Adaptive SuperTrendOverview:

Introducing the Entropy-Based Adaptive SuperTrend – a groundbreaking trading indicator designed to adapt dynamically to market conditions using market entropy. This enhanced SuperTrend indicator adjusts its sensitivity according to the level of chaos (or order) in price movements, providing more stable signals during volatile periods and more responsive signals when the market becomes orderly.

Key Features:

Entropy-Adaptive Mechanism: By incorporating an entropy measure, this indicator estimates the degree of unpredictability in the market. During high entropy periods (more chaotic), signals are made less sensitive, while during low entropy periods, the indicator reacts more quickly to price changes.

Adaptive ATR Multiplier: Unlike traditional SuperTrend indicators that use a fixed ATR multiplier, this version calculates a dynamic ATR multiplier based on the entropy score, ensuring more flexibility and adaptability in setting stop levels.

Visual Clarity: The indicator is overlayed on the price chart with customizable visual elements. The bullish and bearish trends are color-coded for ease of use, and optional entry signals ("L" for long and "S" for short) are plotted to clearly mark potential entry opportunities.

Alerts for Key Opportunities : Never miss an opportunity with built-in alerts for buy and sell signals. Traders can easily configure these alerts to be notified instantly when market conditions trigger a new trend.

How It Works:

Entropy Calculation: The entropy of the price data is calculated over a user-defined period, giving an indication of the degree of randomness in the price movements. The result is then smoothed to reduce noise and create a meaningful trend indication.

Dynamic ATR Adjustment: The ATR (Average True Range) multiplier, which controls the distance of the trailing stop, is adjusted based on the entropy score. This allows the SuperTrend line to widen in chaotic times, reducing false signals, while tightening in orderly times, allowing quicker trend captures.

Parameters Explained:

Entropy Settings: Control the sensitivity of entropy calculations, including the look-back period, number of bins for price distribution, and smoothing length.

Adaptive Settings: Adjust how the indicator adapts to different levels of entropy, including the adaptation period and the filtering weight.

SuperTrend Settings : Customize the ATR period and the dynamic multiplier range to fine-tune the trailing stops for your trading style.

Visual Settings: Choose your preferred colors for bullish and bearish trends, and decide if you want the entry labels displayed directly on the chart.

Use Cases:

Swing Traders can utilize the indicator to capture trend reversals while filtering out the noise during high entropy periods.

Intraday Traders can adapt the settings for shorter time frames to benefit from dynamic adjustments that reduce overtrading and false signals.

Risk Management: The entropy-based adaptive feature provides an edge in risk management by reducing sensitivity during times of increased chaos, thus helping to limit unnecessary trades.

How to Use It:

Look for entry labels ("L" for long, "S" for short) to identify potential opportunities.

Use the color-coded trendlines to determine market bias: greenish hue for bullish trends, reddish hue for bearish trends.

Customize the input settings to align with your preferred market timeframe and risk profile.

Alerts & Notifications:

Built-in alerts notify you of significant trend changes. Simply enable these alerts to receive updates when a new long or short opportunity is detected, helping you stay ahead without needing to watch the screen constantly.

Customization Tips:

Longer Timeframes : Increase the Entropy Period to better capture macro trends in high timeframe charts.

Higher Volatility Markets: Increase the ATR Max Multiplier to ensure stops are set farther away during high entropy.

Lower Volatility Markets: Use a lower ATR Base Multiplier and tighter entropy thresholds to capture rapid price movements.

Final Thoughts:

The Entropy-Based Adaptive SuperTrend indicator merges traditional trend-following logic with an adaptive mechanism driven by market entropy, aiming to address the challenges of whipsaws and false signals common in conventional SuperTrend setups. This indicator offers an intelligent and flexible way to track market trends, suitable for both beginners and experienced trade

Heikin Line - TB365Heikin Line - An Enhanced Smoothed Heiken Ashi Overlay

Built on the foundation of TheBacktestGuy’s Smoothed Heiken Ashi indicator, Heikin Line takes trend analysis to the next level with versatile enhancements and adaptable settings.

This indicator offers selectable moving averages both before and after Heiken Ashi (HA) calculation, adding an additional layer of smoothness to traditional HA candles.

Key Features:

Trend Identification: Detects short and long-term trend directions with greater clarity.

Dynamic Support and Resistance: Not limited to a single line, Heikin Line creates a dynamic support/resistance zone, offering a visual “height” that adjusts with market shifts.

Trailing Stop: Effective as a trailing stop for enhanced risk management.

Trend Reversal Detection: Quickly identifies potential reversals when price crosses above or below the Heiken Ashi candle.

Improvements:

Trend Strength Visualization: Uses a cord-like appearance to reflect trend strength, making it easier to spot strong or weak trends.

Quick Reversal Detection: Enhanced responsiveness to detect rapid market reversals.

Easy Integration: Seamlessly combines with other indicators for a comprehensive trading setup.

With numerous moving average options, Heikin Line is adjustable to suit various market conditions and trading styles. Additionally, it leverages my TAExt library, so you can use it within your own strategies for added versatility.

PineConnectorLibrary "PineConnector"

This library is a comprehensive alert webhook text generator for PineConnector. It contains every possible alert syntax variation from the documentation, along with some debugging functions.

To use it, just import the library (eg. "import ZenAndTheArtOfTrading/PineConnector/1 as pc") and use pc.buy(licenseID) to send an alert off to PineConnector - assuming all your webhooks etc are set up correctly.

View the PineConnector documentation for more information on how to send the commands you're looking to send (all of this library's function names match the documentation).

all()

Usage: pc.buy(pc_id, freq=pc.all())

Returns: "all"

once_per_bar()

Usage: pc.buy(pc_id, freq=pc.once_per_bar())

Returns: "once_per_bar"

once_per_bar_close()

Usage: pc.buy(pc_id, freq=pc.once_per_bar_close())

Returns: "once_per_bar_close"

na0(value)

Checks if given value is either 'na' or 0. Useful for streamlining scripts with float user setting inputs which default values to 0 since na is unavailable as a user input default.

Parameters:

value (float) : The value to check

Returns: True if the given value is 0 or na

getDecimals()

Calculates how many decimals are on the quote price of the current market.

Returns: The current decimal places on the market quote price

truncate(number, decimals)

Truncates the given number. Required params: mumber.

Parameters:

number (float) : Number to truncate

decimals (int) : Decimal places to cut down to

Returns: The input number, but as a string truncated to X decimals

getPipSize(multiplier)

Calculates the pip size of the current market.

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

toWhole(number)

Converts pips into whole numbers. Required params: number.

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips. Required params: number.

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

debug(txt, tooltip, displayLabel)

Prints to console and generates a debug label with the given text. Required params: txt.

Parameters:

txt (string) : Text to display

tooltip (string) : Tooltip to display (optional)

displayLabel (bool) : Turns on/off chart label (default: off)

Returns: Nothing

order(licenseID, command, symbol, parameters, accfilter, comment, secret, freq, debug)

Generates an alert string. Required params: licenseID, command.

Parameters:

licenseID (string) : Your PC license ID

command (string) : Command to send

symbol (string) : The symbol to trigger this order on

parameters (string) : Other optional parameters to include

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: An alert string with valid PC syntax based on supplied parameters

market_order(licenseID, buy, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a market entry alert with relevant syntax commands. Required params: licenseID, buy, risk.

Parameters:

licenseID (string) : Your PC license ID

buy (bool) : true=buy/long, false=sell/short

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A market order alert string with valid PC syntax based on supplied parameters

buy(licenseID, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a market buy alert with relevant syntax commands. Required params: licenseID, risk.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A market order alert string with valid PC syntax based on supplied parameters

sell(licenseID, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a market sell alert with relevant syntax commands. Required params: licenseID, risk.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A market order alert string with valid PC syntax based on supplied parameters

closeall(licenseID, comment, secret, freq, debug)

Closes all open trades at market regardless of symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closealleaoff(licenseID, comment, secret, freq, debug)

Closes all open trades at market regardless of symbol, and turns the EA off. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closelong(licenseID, symbol, comment, secret, freq, debug)

Closes all long trades at market for the given symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closeshort(licenseID, symbol, comment, secret, freq, debug)

Closes all open short trades at market for the given symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closelongshort(licenseID, symbol, comment, secret, freq, debug)

Closes all open trades at market for the given symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closelongbuy(licenseID, risk, symbol, comment, secret, freq, debug)

Close all long positions and open a new long at market for the given symbol with given risk/contracts. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : Risk or contracts (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closeshortsell(licenseID, risk, symbol, comment, secret, freq, debug)

Close all short positions and open a new short at market for the given symbol with given risk/contracts. Required params: licenseID, risk.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : Risk or contracts (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

newsltplong(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any open long trades on the given symbol with the given values. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

newsltpshort(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any open short trades on the given symbol with the given values. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closelongpct(licenseID, symbol, comment, secret, freq, debug)

Close a percentage of open long positions (according to EA settings). Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closeshortpct(licenseID, symbol, comment, secret, freq, debug)

Close a percentage of open short positions (according to EA settings). Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closelongvol(licenseID, risk, symbol, comment, secret, freq, debug)

Close all open long contracts on the current symbol until the given risk value is remaining. Required params: licenseID, risk.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : The quantity to leave remaining

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

closeshortvol(licenseID, risk, symbol, comment, secret, freq, debug)

Close all open short contracts on the current symbol until the given risk value is remaining. Required params: licenseID, risk.

Parameters:

licenseID (string) : Your PC license ID

risk (float) : The quantity to leave remaining

symbol (string) : Symbol to act on (defaults to current symbol)

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

limit_order(licenseID, buy, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a limit order alert with relevant syntax commands. Required params: licenseID, buy, price, risk.

Parameters:

licenseID (string) : Your PC license ID

buy (bool) : true=buy/long, false=sell/short

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A limit order alert string with valid PC syntax based on supplied parameters

buylimit(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a buylimit order alert with relevant syntax commands. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A limit order alert string with valid PC syntax based on supplied parameters

selllimit(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a selllimit order alert with relevant syntax commands. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A limit order alert string with valid PC syntax based on supplied parameters

stop_order(licenseID, buy, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a stop order alert with relevant syntax commands. Required params: licenseID, buy, price, risk.

Parameters:

licenseID (string) : Your PC license ID

buy (bool) : true=buy/long, false=sell/short

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

buystop(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a buystop order alert with relevant syntax commands. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

sellstop(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Generates a sellstop order alert with relevant syntax commands. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancel_neworder(licenseID, order, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Cancel + place new order template function.

Parameters:

licenseID (string) : Your PC license ID

order (string) : Cancel order type

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancellongbuystop(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Cancels all long orders with the specified symbol and places a new buystop order. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancellongbuylimit(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Cancels all long orders with the specified symbol and places a new buylimit order. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancelshortsellstop(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Cancels all short orders with the specified symbol and places a sellstop order. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancelshortselllimit(licenseID, price, risk, sl, tp, betrigger, beoffset, spread, trailtrig, traildist, trailstep, atrtimeframe, atrperiod, atrmultiplier, atrshift, atrtrigger, symbol, accfilter, comment, secret, freq, debug)

Cancels all short orders with the specified symbol and places a selllimit order. Required params: licenseID, price, risk.

Parameters:

licenseID (string) : Your PC license ID

price (float) : Price or pips to set limit order (according to EA settings)

risk (float) : Risk quantity (according to EA settings)

sl (float) : Stop loss distance in pips or price

tp (float) : Take profit distance in pips or price

betrigger (float) : Breakeven will be activated after the position gains this number of pips

beoffset (float) : Offset from entry price. This is the amount of pips you'd like to protect

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips

trailtrig (float) : Trailing stop-loss will be activated after a trade gains this number of pips

traildist (float) : Distance of the trailing stop-loss from current price

trailstep (float) : Moves trailing stop-loss once price moves to favourable by a specified number of pips

atrtimeframe (int) : ATR Trailing Stop timeframe, only updates once per bar close. Options: 1, 5, 15, 30, 60, 240, 1440

atrperiod (int) : ATR averaging period

atrmultiplier (float) : Multiple of ATR to utilise in the new SL computation, default = 1

atrshift (int) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default = 0

atrtrigger (int) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default = 0 (instant)

symbol (string) : The symbol to trigger this order on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment (maximum 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A stop order alert string with valid PC syntax based on supplied parameters

cancellong(licenseID, symbol, accfilter, comment, secret, freq, debug)

Cancels all pending long orders with the specified symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A cancel long alert command

cancelshort(licenseID, symbol, accfilter, comment, secret, freq, debug)

Cancels all pending short orders with the specified symbol. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: A cancel short alert command

newsltpbuystop(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any pending buy stop orders on the given symbol. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

newsltpbuylimit(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any pending buy limit orders on the given symbol. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

newsltpsellstop(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any pending sell stop orders on the given symbol. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

newsltpselllimit(licenseID, sl, tp, symbol, accfilter, comment, secret, freq, debug)

Updates the stop loss and/or take profit of any pending sell limit orders on the given symbol. Required params: licenseID, sl and/or tp.

Parameters:

licenseID (string) : Your PC license ID

sl (float) : Stop loss pips or price (according to EA settings)

tp (float) : Take profit pips or price (according to EA settings)

symbol (string) : Symbol to act on (defaults to current symbol)

accfilter (float) : Optional minimum account balance filter

comment (string) : Optional comment to include (max 20 characters)

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

eaoff(licenseID, secret, freq, debug)

Turns the EA off. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

eaon(licenseID, secret, freq, debug)

Turns the EA on. Required params: licenseID.

Parameters:

licenseID (string) : Your PC license ID

secret (string) : Optional secret key (must be enabled in dashboard)

freq (string) : Alert frequency. Default = "all", options = "once_per_bar", "once_per_bar_close" and "none"

debug (bool) : Turns on/off debug label

Returns: The required alert syntax as a string

Confluence StrategyOverview of Confluence Strategy

The Confluence Strategy in trading refers to the combination of multiple technical indicators, support/resistance levels, and chart patterns to identify high-probability trading opportunities. The idea is that when several indicators agree on a price movement, the likelihood of that movement being successful increases.

Key Components

Technical Indicators:

Moving Averages (MA): Commonly used to determine the trend direction. Look for crossovers (e.g., the 50-day MA crossing above the 200-day MA).

Relative Strength Index (RSI): Helps identify overbought or oversold conditions. A reading above 70 may indicate overbought conditions, while below 30 suggests oversold.

MACD (Moving Average Convergence Divergence): Useful for spotting changes in momentum. Look for MACD crossovers and divergence from price.

Support and Resistance Levels:

Identify key levels where price has historically reversed. These can be drawn from previous highs/lows, Fibonacci retracement levels, or psychological price levels.

Chart Patterns:

Patterns like head and shoulders, double tops/bottoms, or flags can indicate potential reversals or continuations in price.

Strategy Implementation

Set Up Your Chart:

Add the desired indicators (e.g., MA, RSI, MACD) to your TradingView chart.

Mark significant support and resistance levels.

Identify Confluence Points:

Look for situations where multiple indicators align. For instance, if the price is near a support level, the RSI is below 30, and the MACD shows bullish divergence, this may signal a buying opportunity.

Entry and Exit Points:

Entry: Place a trade when your confluence conditions are met. Use limit orders for better prices.

Exit: Set profit targets based on resistance levels or use trailing stops. Consider the risk-reward ratio to ensure your trades are favorable.

Risk Management:

Always implement stop-loss orders to protect against unexpected market moves. Position size should reflect your risk tolerance.

Example of a Confluence Trade

Setup:

Price approaches a strong support level.

RSI shows oversold conditions (below 30).

The 50-day MA is about to cross above the 200-day MA (bullish crossover).

Action:

Enter a long position as the conditions align.

Set a stop loss just below the support level and a take profit at the next resistance level.

Conclusion

The Confluence Strategy can significantly enhance trading accuracy by ensuring that multiple indicators support a trade decision. Traders on TradingView can customize their indicators and charts to fit their personal trading styles, making it a flexible approach to technical analysis.

Stochastic RSI OHLC StrategyThe script titled "Stochastic RSI High Low Close Bars" is a versatile trading strategy implemented in Pine Script, designed for TradingView. Here's an overview of its features:

Description

This strategy leverages the Stochastic RSI to determine entry and exit signals in the market, focusing on high, low, and close values of the indicator. It incorporates various trading styles, stop-loss mechanisms, and multi-timeframe analysis to adapt to different market conditions.

Key Features

Stochastic RSI Analysis:

Uses the Stochastic RSI to identify potential entry points for long and short positions.

Tracks high, low, and close values for more granular analysis.

Multiple Trading Styles:

Supports diverse trading styles like Volume Color Swing, RSI Divergence, RSI Pullback, and more.

Allows switching between these styles to suit market dynamics.

Session-Based Trading:

Offers session control, limiting trades to specific hours (e.g., NY sessions).

Can close all positions at the end of the trading day.

Stop-Loss and Take-Profit Mechanisms:

Includes both static and dynamic stop-losses, with options for time-based stops, trailing stops, and momentum-based exits.

Customizable take-profit levels ensure efficient trade management.

Volume Analysis:

Integrates volume indicators to add a bias for trade entries and exits, enhancing signal reliability.

Multi-Timeframe Integration:

Employs multi-timeframe RSI analysis, allowing the strategy to capture broader trends and optimize entries.

This script is designed to provide flexibility and adaptability, making it useful for different trading strategies and market conditions. It is suitable for traders looking to refine their entries and exits with a focus on the Stochastic RSI.

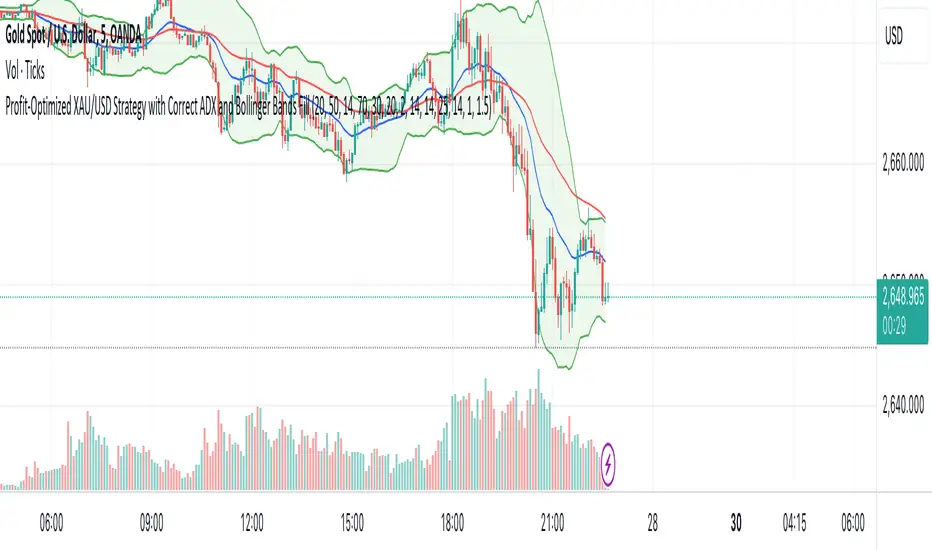

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

Negroni Opening Range StrategyStrategy Summary:

This tool can be used to help identify breakouts from a range during a time-zone of your choosing. It plots a pre-market range, an opening range, it also includes moving average levels that can be used as confluence, as well as plotting previous day SESSION highs and lows.

There are several options on how you wish to close out the trades, all described in more detail below.

Back-testing Inputs:

You define your timezone.

You define how many trades to open on any given day.

You decide to go: long only, short only, or long & short (CAREFUL: "Long & Short" can open trades that effectively closes-out existing ones, for better AND worse!)

You define between which times the strategy will open trades.

You define when it closes any open trades (preventing overnight trades, or leaving trades open into US data times!!).

This hopefully helps make back-testing reflect YOUR trading hours.

NOTE: Renko or Heikin-Ashi charts

For ALL strategies, don’t use Renko or Heikin-Ashi charts unless you know EXACTLY the implications.

Specific to my strategy, using a renko chart can make this 85-90% profitable (I wish it was!!) Although they can be useful, renko charts don’t always capture real wicks, so the renko chart may show your trade up-only but your broker (who is not using renko!!) will have likely stopped you out on a wick somewhere along the line.

NOTE: TradingView ‘Deep backtesting’

For ALL strategies, be cynical of all backtesting (e.g. repainting issues etc) as well as ‘Deep backtesting’ results.